Examine This Report about Second Mortgage Vancouver

Table of ContentsSome Known Facts About Second Mortgage Vancouver.Some Known Factual Statements About Foreclosure Loans 5 Simple Techniques For Loans VancouverA Biased View of Foreclosure Loans

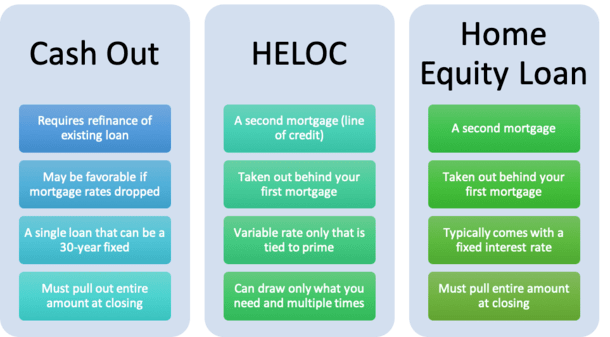

If you are not able to pay the car loan back, you might lose your residence to foreclosure. Are Residence Equity Loans Tax Obligation Deductible? The interest paid on a residence equity financing can be tax deductible if the earnings from the funding are made use of to "acquire, construct, or considerably boost" your house - Home Equity Loans BC.Just How Much House Equity Lending Can I get? For well-qualified debtors, the restriction of a home equity finance is the amount that gets the customer to a combined loan-to-value (CLTV) of 90% or less. This means the total of the equilibriums on the home mortgage, any existing HELOCs, any existing residence equity finances, and also the brand-new home equity financing can not be greater than 90% of the appraised value of the home.

You can have both a HELOC and also a home equity funding at the exact same time, offered you have enough equity in your house, as well as the income as well as credit score to get approved for both. The Bottom Line A residence equity car loan can be a better option economically than a HELOC for those that know exactly just how much equity they need to draw out as well as want the security of a set passion rate.

Among the advantages of homeownership is being able to use the equity in your home and use it as security for a car loan when money is required to pay for significant costs such as home renovations or financial obligation consolidation. Funded in a lump sum and also paid back over 5 to 30 years at a set rates of interest, house equity financings can be a good option for these kinds of big money demands.

Some Known Facts About Second Mortgage Vancouver.

Here are the advantages and disadvantages of home equity finances. Secret benefits of residence equity finances, Those that get residence equity financings might find there are numerous advantages versus other forms of borrowing. Taken care of interest, Unlike a residence equity line of credit history (HELOC), which includes a variable rate of interest that can increase all of a sudden at any kind of time, the passion price on a house equity financing is dealt with for the life of the funding."When you get a house equity funding, right from the beginning, you will recognize precisely just how much you'll need to pay back each month and also what the rate of interest will be," claims Sam Eberts, jr partner with economic services strong Dugan Brown.

Long repayment terms, The repayment terms on house equity financings can my site be as long as 20 years. This reality, coupled with reduced rate of interest than unsafe financings can convert into a really inexpensive month-to-month repayment installation. Possible tax-deductible interest, One more prospective advantage of house equity financings is the tax write-off.

Getting a house equity loan typically needs having in between 15 percent to 20 percent in equity in your property. A home equity car loan is connected to your house. If you choose to sell see this page the house, you will be required to repay the funding."In a lot of cases, you might have the ability to use the proceeds of your residence sale to pay off both loans," says Sterling.

:max_bytes(150000):strip_icc()/dotdash_Final_Home_Equity_Loan_vs_HELOC_What_the_Difference_Apr_2020-01-af4e07d43f454096b1fbad8cfe448115.jpg)

Examine This Report about Mortgages Vancouver

HELOCs, Both a residence equity funding and a home equity credit line (HELOC) utilize your home as collateral when obtaining cash. However, there are likewise several differences between these 2 economic products, making it essential to do your research study and understand which one is genuinely appropriate for your requirements and monetary image.

On top of that, this option includes a fixed rate of interest price for the life of the financing and also dealt with monthly payments, which can be a safer wager for those on a tight budget."Home equity fundings offer you the safety of understanding your precise regular monthly repayments," says Sterling, of Georgia's Own. HELOCA HELOC is a revolving line of credit similar to a charge card.

/se-bcd005f97ba74fc88523b4f99a995ee9.jpg)

Nonetheless, you should assume thoroughly regarding whether you fit using your house as collateral before waging this sort of funding bearing in mind that if somehow you skip, you might lose your house.

Top Guidelines Of Loans Vancouver

Alternatives to a house equity lending, A home equity car loan isn't your only option when you need money. The advantage of this course is that you're not devoting to obtaining the whole sum, so you don't automatically have to start paying interest on it.

Picture you're taking a look at what you believe will certainly be a $30,000 residence repair. If you obtain a $30,000 house equity car loan, you'll be on the hook for interest on that whole $30,000. If you protect a $30,000 HELOC, but your repair just winds up costing $25,000, you'll avoid paying passion on the continuing to be $5,000 (presuming you don't borrow it for one more purpose).

You borrow even more than the amount of your impressive residence car loan balance. That method, you obtain the difference in money as well as use that cash as you please., you may take article out a brand-new loan worth $180,000 - Second Mortgage Vancouver.